Bob Fraser – Sales & Service, Genesus Ontario

Canada – Waiting for China (or Godot)

I reference the famous Theatre of the Absurd play by Samuel Beckett, Waiting for Godot* because here in Canada our wait for better days from China is feeling all to similar. Like for Godot we wait and hope but seemingly he never shows up.

*Waiting for Godot” is a play by Samuel Beckett, in which two characters, Vladimir (Didi) and Estragon (Gogo), wait for the arrival of someone named Godot who never arrives, and while waiting they engage in a variety of discussions and encounter three other characters.

So it has been with China. With the devastation of ASF in China and beyond conventional wisdom seems to be something equating to 25% of the world’s pigs are gone!

Simple Economics 101 would say that that fact should certainly do you some good. However here in Canada, we continue to wait and hope. Approximately a year ago March we had a nice futures lead speculative run. Ultimately proved a tease and relatively short-lived.

Since that time the market has mostly gone the wrong direction. With geopolitical issues leading to tariffs and for a time last year a straight-out ban for Canada. We seemingly no more than get that lifted and we have coronavirus adding insult to injury. Theatre of the Absurd indeed.

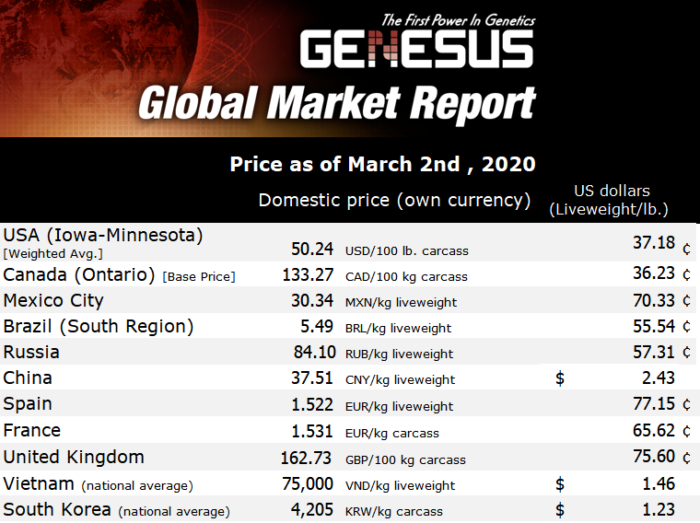

From OMAFRA

Monthly Hog Market Facts – Net Returns Farrow to Finish 2019

January (-$29.79), February (-$33.43), March (-$27.16), April $36.50, May $47.33, June $29.96 – First 6 months $3.90

July $6.27, August $22.33, September (-$32.26), October (-$25.54), November (-$27.84), December (-$30.09) – for year 2019 (-$5.46)

January 2020 (-$29.41)

As you can see above more negative than positive numbers and a negative average for the year, bleeding continues. It makes one not even want to consider where we might be without exports to China.

“Canada exported about 63% of its pork production last year. That does not count live exports to the United States. The export share compares to 61% in 2010 and just 40% in 2000. U.S. export share of production last year was 23% compared to 19% in 2010 and 7% in 2000.”

Kevin Grier, Market Analysis and Consulting

Canadian Pork Market Report, February 2020 –

As one can see Canada has long been export-dependent for its fortunes in the

pork business and increasingly so. The US is now increasingly discovering

the pros and cons of that game. As Kevin Grier further outlines below this is a

hard game and as of late the EU appears to be the major winner

Losing Export Share

“In 2010 Canada supplied 20% of global imports. In 2019 that share had declined to just 15% of the world’s imports being supplied by Canada. Canada’s losses were broad-based losing share to all major markets except China and Mexico.

Kevin Grier, Market Analysis and Consulting

Interestingly, despite the massive growth in U.S. production, it supplied about a third of global import demand in 2010 and about the same in 2019. The EU was the big global export leader as its tonnage more than doubled. It supplied 29% of world import demand in 2010 and 41% last year.”

Canadian Pork Market Report, February 2020 –

It appears that as the North American industry becomes more and more export-driven the volatility increases. Particularly for the producer at least. This seems to be part of the push for ever-increasing integration – placing pork as the profit centre and pig production as a cost centre.

Here in Ontario, Progressive Pork Producers (3P) recognized this trend some 20+ years ago. They chose to integrate up to Conestoga Meats. A producer coop owning a plant that now slaughters 38,000 hogs per week. They share the packer margin that is adding fifty dollars plus presently to the above margins. After many challenging years looks like a pretty good idea presently.

Manitoba has integrated the other direction, down. Maple Leaf Foods has a considerable integrated production base. Hylife, a large production base with a sizable packing plant in Neepawa MB, has just been purchased 51% by CP, a massive integrated Thai company. Canada, whether the integration is up or down, appears to be rapidly following the US model. Whence the independent producer?

Categorised in: Featured News, Global Markets

This post was written by Genesus