Where we at? Where are we going?

This past week a year ago US 53-54% lean hogs were averaging 69¢ lb; this year, this past week 73¢ lb – 4¢ higher, or about $8 per head to the good

A year ago, U.S. cash 40lb feeder pig were averaging $72; this week, this year they are averaging $ 88 – a difference of $16

The US marketed 2,438,000 this week. Year to date 11,707,000 last year 11,499,000 – a difference of 204,000 head or 1.8%

This year, last week the Average Market Hog weighed 285.5 lbs (Iowa-S Minnesota); last year, same week, 282.1 lbs – A significant difference of 3.4 lbs

Our observation is that stronger prices for market hogs and feeder pigs, despite increased production, is a true reflection of good demand

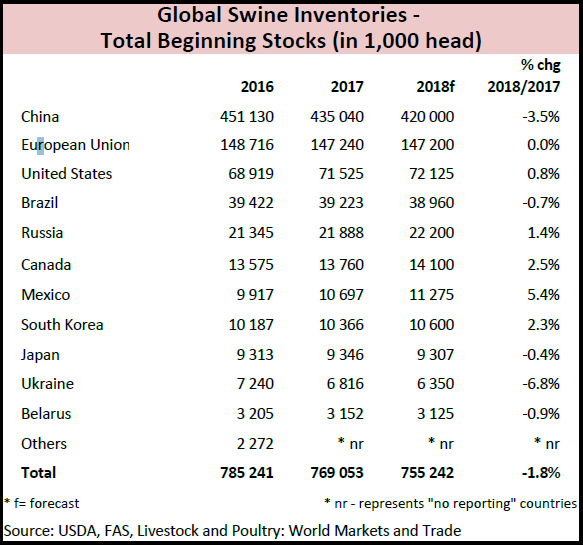

Global Swine Inventory

Below is a chart showing Global Swine Inventories from the USDA. Of note; total inventory is estimated to be -1.8% then the previous year. Less is not more!

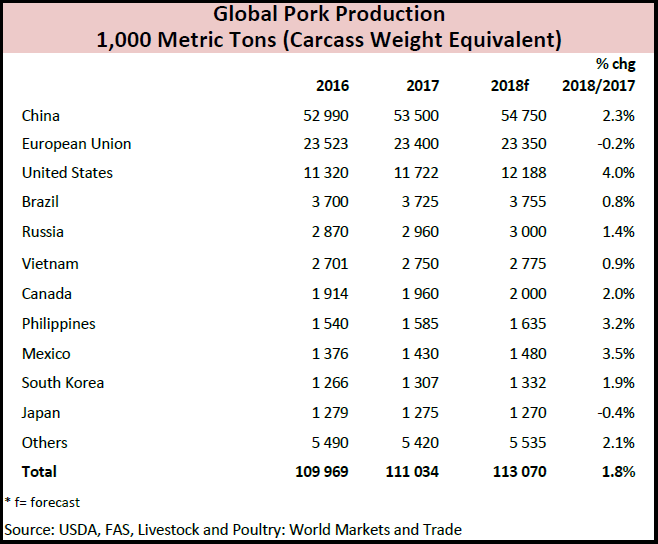

Global Pork Production

The world chart above below, estimated world pork production by the USDA – an increase of 1.8% in total production. The worlds human population increases 1.1% per year (83 million people). Population increase, coupled with greater pork demand, is helping to keep most markets profitable around the world.

This week will attend the AMVECAJ Pork Congress, held in Tepatitlán, Mexico. We will be speaking and will file our observations on the Mexican Industry in next weeks commentary

Categorised in: Featured News, Pork Commentary

This post was written by Genesus