Pork Commentary

Jim Long, President-CEO Genesus Inc.

March 13, 2017

United States and Canada Inventory Up 3%

Twice a year, the United States and Canadian Swine Inventories are combined together. It is a significant number, as the two countries are in essence one large inventory and production base. It’s a virtually integrated continental market. Last week, the latest report was released.

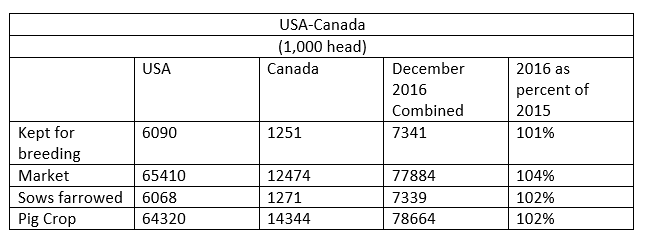

United States and Canadian Inventory of all hogs and pigs for December 2016 was 85.2 million head. This was up 3% from December 2015, and up 5% from December 2014. The breeding inventory, at 7.34 million head, was up 1% from a year ago and 2% from 2014. Market hog inventory, at 77.9 million head, was up 4% from last year and up 6% from 2014. The semi-annual pig crop at 78.7 million head was up 2% from 2015, and up 5% from 2014. Sow farrowing during this period totalled 7.34 million, up 2% from last year and up 1 % from 2014.

The numbers show the combined breeding herd has climbed some 59,000 sows year over year. Not exactly a massive expansion. In that number is an increase of 14,000 in Canada year over year. What we find interesting is the combined pig crop was up 2% or about 1.8 million head year over year. Divided by 26 weeks, that would be about 70,000 more per week.

With the new US harvesting plants coming on stream when this pig crop is going to market, we calculate that the new plants will increase capacity almost 200,000 head a week. 70,000 for 200,000, seems to us packer capacity will be plentiful and this should support hog prices.

Other Observations

- US Pork Exports continued strong in January. Mexico continues to be a superstar, taking 35.8% more than the same month a year ago. The total pork exports to all countries up 19% from January 2017, total was 457 million pounds. Other major players other than Mexico were South Korea (up 33% at 49 million pounds), and of course Japan at 98 million pounds. China was 34 million, about the same as a year ago. China’s huge import increases have mostly been captured by European suppliers.

- There have been a couple Avian Flu outbreaks in the USA in chicken broiler flocks in the last week. Flocks have been destroyed. South Korean pork imports, as you saw earlier, have jumped. Genesus is a major supplier of swine genetics to South Korea. We have continual contact with that market. Avian flu in South Korea has destroyed in the last few months 35% of the chicken, egg, and broiler flocks. There is not only a shortage of poultry meat and eggs, but some consumers are fearful of dying if they eat poultry. Last week, South Korean hog price was 4,707 KRW/kg, or $1.31 US liveweight/lb. That’s $350 USD for a market hog. What happens if Avian Flu gets rolling into US broiler flocks? Doubt it, but if it does, a Black Swan moment.

- Shoot the messenger. As you have read in this commentary, Topigs-Norsvin had a financial loss of $6.91 million US in their last fiscal year. This we had verified by senior Topigs-Norsvin executives. This past week, Genesus personnel were confronted by Topigs-Norsvin associates complaining profusely that we had the audacity to tell the world of their financial situation. Not that it wasn’t true, but that we had the nerve to tell the truth. Indeed, it must be hard for Topigs-Norsvin, who claims to be the second largest genetic company in the world, to explain to its stakeholders how they lost $6.91 million USD while the largest genetic company (PIC) had profits in the $50 million USD range in the same industry. Shoot the messenger – Topigs-Norsvin people should get a mirror, focus on their own reality.

Categorised in: Featured News, Pork Commentary

This post was written by Genesus